For the first time in several years, the yield curve is beginning to steepen and that shift is quietly creating new opportunities for credit unions.

Why this matters now

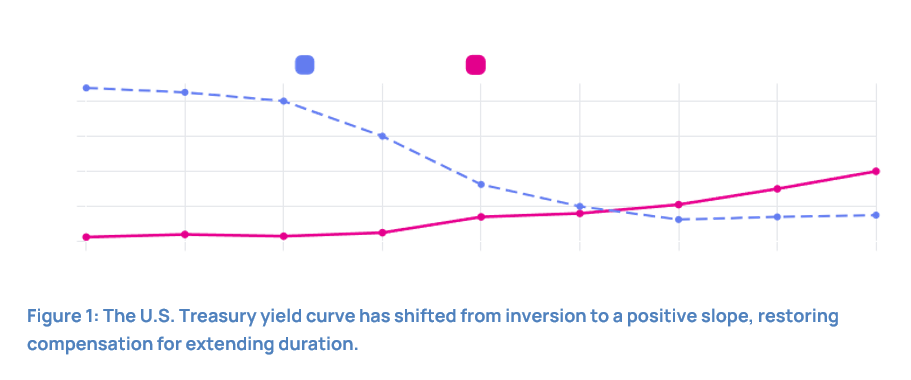

From late 2022 through the end of 2025, credit unions operated in an unusual environment. Short term interest rates were higher than longer duration rates, making cash and overnight investments the most attractive option. In many cases, holding cash actually produced better returns than investing further out on the curve. As a result, many credit unions maintained ample liquidity but limited incentive to deploy it.

That dynamic is now changing.

A shift back toward longer-term value

As the yield curve steepens, longer-term investments are once again offering higher yields than short-term options. While the difference may appear modest, about 35 basis points between cash and five-year Treasuries, the shift is meaningful. More importantly, this shift allows credit unions to lock in today’s rates rather than remain exposed to declining yields in the future.

For finance leaders, this is a critical distinction:

- Cash offers flexibility, but income can reset quickly if rates fall

- Longer-term investments provide greater income stability and earnings visibility

Managing reinvestment risk

Over the past several years, reinvestment risk hasn’t been a primary concern but as the rate environment evolves, that risk is becoming more relevant.

After several years of deposit inflows, slowed loan demand and cautious portfolio positioning, many credit unions continue to carry elevated liquidity relative to longer term deployment opportunities.

Holding excess liquidity for extended periods creates challenges when the rate environment shifts. If short term rates decline, earnings on overnight investments will follow. For credit unions carrying higher cash balances, this can quickly pressure net interest income.

The return of positive term premium provides credit unions with new opportunities. By gradually reallocating a portion of liquidity into intermediate term investments, credit unions can:

- Preserve yield levels for a longer period

- Reduce sensitivity to short-term rate movements

- Improve consistency in future earnings

A practical path forward

The current environment doesn’t require a dramatic shift, it calls for a measured, strategic approach. Credit unions can begin redeploying liquidity incrementally, staying within existing policies while better aligning their investment strategy with longer-term balance sheet goals. For those seeking additional yield without adding unnecessary complexity, certain Agency CMBS structures, such as Fannie Mae DUS and Freddie K bonds, can complement traditional Treasury allocations. For example, a Fannie Mae DUS bond with an average life of approximately 4.8 years is currently offered at a spread of plus 21 basis points, translating to a yield of roughly 4.54%.

These investments offer:

- Strong credit quality backed by government-sponsored enterprises

- Predictable, structured cash flows

- Additional yield enhancement over comparable Treasuries

When combined with intermediate Treasuries, this approach can deliver meaningful yield improvement while maintaining simplicity and transparency, an appealing outcome in an environment where rate cuts remain a longer-term possibility.

A renewed opportunity for balance sheet strategy

After several years of limited options, the return of a positive yield curve creates a more constructive environment for investment decision making. For credit unions holding elevated cash balances, the question is not whether to explore in longer-term investments farther out on the yield curve but how to do so in a way that balances yield, risk and long-term performance.

A more strategic approach starts with the right partner

Navigating a changing rate environment requires more than just identifying opportunities, it requires a strategy that aligns with your credit union’s balance sheet, risk tolerance and long-term objectives.

Catalyst offers deep expertise in investment strategy, balance sheet management and portfolio construction. Our team works alongside credit unions to evaluate options, model outcomes and implement solutions that support both current earnings and future stability.

Whether you’re looking to redeploy excess liquidity, manage interest rate risk or enhance portfolio performance, Catalyst can help you take a deliberate, informed approach.

Connect with our team to explore how we can support your balance sheet strategy.

All securities are offered through CU Investment Solutions LLC (ISI). The home office of ISI is located at 8500 W. 110th St., Overland Park, KS 66210. ISI is registered with the Securities and Exchange Commission (SEC) as a broker-dealer under the Securities Exchange Act of 1934. ISI also is registered in the state of Kansas as an investment advisor. Member of FINRA and SIPC. All investments carry risk; please speak with your representative to gain a full understanding of said risks. Securities offered by ISI are not insured by the FDIC or NCUSIF and may lose value. All opinions, prices and yields are subject to change without notice.